52-Week Money Saving Challenge: Free Printable Trackers to Hit Your Savings Goals

You set a savings goal. You feel motivated for the first two weeks. Then life happens — an unexpected bill, a weekend trip, a "treat yourself" moment — and suddenly your savings account looks exactly the same as it did last month. If this sounds familiar, you are not alone. The problem is not your discipline. The problem is that saving without a visible, trackable system feels invisible. A printable savings challenge tracker changes that — it turns abstract goals into something you can check off, color in, and see growing every single week.

This guide covers how savings challenge trackers work, which challenge method fits your financial situation, and how PrintlyTool's free customizable savings tracker helps you hit your target — whether it's $500, $5,000, or $10,000. No app download. No email registration. Just customize, print, and start saving.

Why Most Savings Plans Fail (and How a Printable Tracker Fixes It)

There are dozens of budgeting apps with savings goal features. Yet according to surveys, over 60% of people who set financial resolutions abandon them by February. The reasons are surprisingly consistent:

- Invisible progress: An app shows you a number. A printed tracker on your fridge shows you 37 out of 52 squares colored in. The visual gap between "almost there" and "barely started" is impossible to ignore.

- Decision fatigue: An app asks you to log in, navigate menus, and update numbers. A printed tracker sits in plain sight with a pen next to it — you fill in one square and you are done.

- No external accountability: Your phone is private. No one sees your app screen. A tracker on the fridge is seen by everyone you live with. That gentle social pressure keeps you going when motivation dips.

- Goal dilution: Apps often let you adjust goals with a swipe. Printed trackers have a fixed total — you committed to $5,000, and that number is staring back at you every day. No easy "let me lower it to $2,000" button.

The most effective system is often the simplest one: a single sheet of paper with a clear target and 52 boxes to fill in.

The 52-Week Challenge: How It Works

The classic 52-week money challenge follows a simple rule: save an amount equal to the week number.

Week 1: save $1. Week 2: save $2. Week 3: save $3. Continue through week 52: save $52. By the end of the year, you will have saved $1,378.

The genius of this system is the ramp-up. The early weeks are trivially easy, which builds the habit. By the time the amounts get meaningful in weeks 40-52, the habit is already wired in and skipping a week feels like breaking a streak.

Who the Classic Challenge Works Best For

- People who have never successfully saved before

- Anyone who finds large monthly savings targets intimidating

- Those paid weekly or bi-weekly who can align savings with payday

How to Adapt the Challenge for Different Goals

The classic $1,378 is a solid starting point, but many people want to save more aggressively. Here are the most popular variants:

$5,000 in 52 Weeks: Start at approximately $51 in week 1 and increase by $2 each week. By week 26, you save about $101. The second half of the year gradually steps back down, keeping the total manageable. This spreads the load more evenly across the year.

$10,000 in 52 Weeks: Double the $5,000 amounts. Start at roughly $100-110 per week early in the year and scale up from there. This requires a higher income baseline but is achievable for dual-income households cutting back on dining out and subscription services.

Reverse 52-Week Challenge: Start with $52 in week 1 and work down to $1 in week 52. This front-loads the hard weeks, which works well if you have higher income early in the year (tax refund season, bonus season) and want easier weeks later.

100-Day Savings Challenge: You commit to saving a fixed amount every day for 100 days. For example, saving $50/day for 100 days gives you $5,000. This is better for people who prefer daily consistency over weekly scaling.

Bi-Weekly Paycheck Challenge: Save roughly $192 per pay period for 26 pay periods to reach $5,000. If you are paid every two weeks, this aligns perfectly with your cash flow.

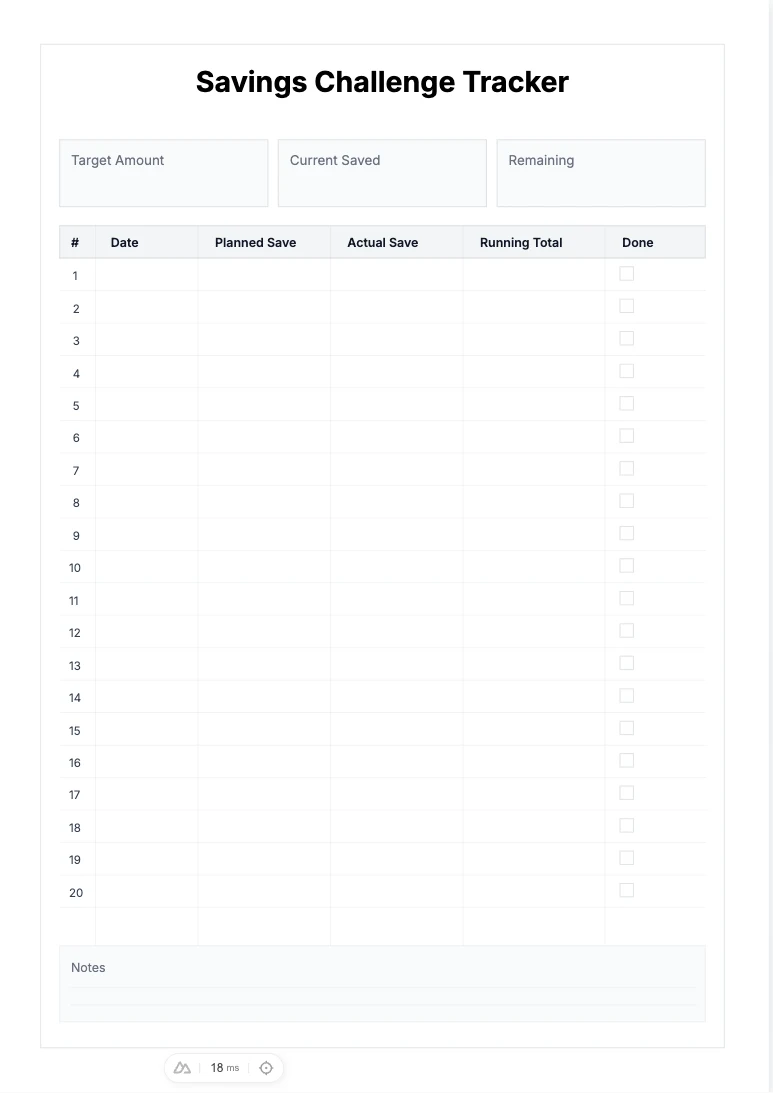

Free printable savings challenge tracker with target, planned, actual, and running-total fields for consistent money-saving habits.

PrintlyTool's savings challenge tracker lets you customize the target amount, choose your challenge style, and print a fresh tracker whenever you need one. Unlike the static PDF downloads found on most finance blogs, you decide the amounts and layout.

How to Use a Savings Challenge Tracker Effectively

A printed tracker works best when you treat it as part of your weekly routine. Here is the system that has worked for thousands of savers:

1. Pick Your Goal and Choose Your Challenge

Be specific. "I want to save more" is not a goal. "I want to save $3,000 for a trip to Japan in November" is a goal. Pick the challenge format that fits:

- $500-$1,500 range → Classic 52-week or reverse challenge

- $3,000-$5,000 range → Modified 52-week with higher increments or 100-day challenge

- $5,000-$10,000 range → $5,000 52-week challenge or bi-weekly paycheck challenge

2. Print It and Put It Where You Cannot Miss It

This sounds obvious but placement matters enormously. Good locations: refrigerator door, bathroom mirror, above your desk, next to your computer monitor. Bad locations: inside a drawer, in a binder you never open, on a bookshelf behind other papers. The tracker must be in a place you pass multiple times a day.

3. Set Up an Automatic Transfer — Then Use the Tracker as a Visual Confirmation

This is the single most important tip. Set up an automatic weekly transfer from your checking account to a separate savings account. Then, every weekend, check that the transfer went through and color in that week's square on the tracker. The automation handles the money; the tracker handles the motivation.

4. Pair It with a Budget to Find the Money

If you look at your current spending and think "I cannot find an extra $50 a week," you need a budget. Specifically, you need to see where your money is currently going before you can redirect it. A household budget template makes this process structured:

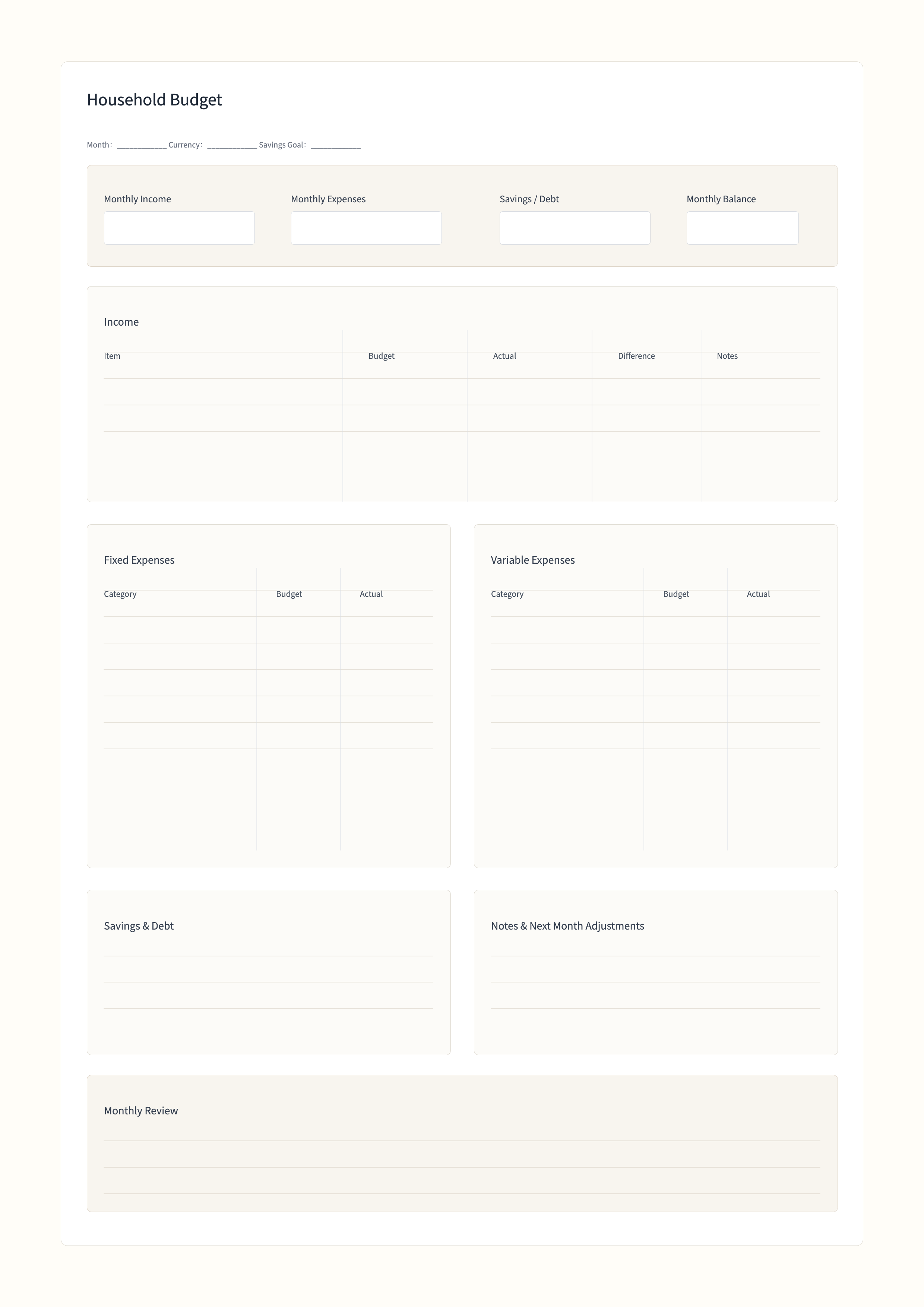

Free printable household budget sheet with sections for income, fixed expenses, variable expenses, savings, and monthly review on one page.

PrintlyTool's household budget template helps you track income, fixed expenses, variable spending, and savings in one place. Use it monthly alongside your savings challenge tracker. When the budget shows you spent $180 on takeout last month, you know exactly where to cut to fund next month's savings.

Week-by-Week: What to Expect on Your Savings Journey

Knowing how the emotional arc of a savings challenge plays out helps you push through the hard parts:

![]()

Weeks 1-8 (The Honeymoon Phase): Amounts are small, motivation is high. You color in squares with enthusiasm. This is the habit-forming stage — focus on consistency, not amount. If you miss a week early, do not double up next week. Just pick up where you left off and accept a slightly smaller final total.

Weeks 9-26 (The Grind): Amounts are now noticeable but not painful — $10 to $25 per week. Motivation may dip. This is when the tracker's physical presence matters most. You see it every day. You remember why you started. Keep going.

Weeks 27-40 (The Push): Amounts are now meaningful — $27 to $40 per week. You might need to make real trade-offs. Cancel one subscription. Cook one extra meal at home per week. Use your budget template to find the money. The end is in sight: two-thirds of the way there.

Weeks 41-52 (The Finish): Amounts peak at $41-$52 per week. This is the toughest stretch but also the most motivating — you can see almost the entire tracker filled in. The visual progress is undeniable. When you color in that very last square, you have $1,378 (or your chosen target) in an account that started at zero. That feeling is worth far more than any single deposit along the way.

What to Do with the Money Once You Have Saved It

A common mistake: completing a savings challenge, feeling proud, and then keeping the money in a regular checking account where it slowly gets spent on nothing in particular. Give your savings a specific job:

| Category | Examples |

|---|---|

| Emergency Fund | Keep 3-6 months of expenses in a high-yield savings account. Start here if you have no safety net. |

| Sinking Fund | Set aside money for predictable annual expenses: car insurance, holiday gifts, property taxes. Your savings challenge can fully fund next year's holiday season. |

| Specific Goal | Vacation, wedding, home down payment, new laptop. Naming the goal keeps you from raiding the fund. |

| Investment | Once you have an emergency fund, consider moving savings challenge money into a Roth IRA or index fund. |

Starting another challenge immediately after finishing one creates a compounding effect: year one builds the habit, year two builds the wealth.

How PrintlyTool's Savings Tracker Is Different

Most "free printable savings challenge" PDFs you find online are pre-set designs — one fixed goal, one fixed color scheme, and often an email signup form to access the download. PrintlyTool takes a different approach:

- Customize your goal amount: Set any target, not just the standard $1,000 or $5,000. If you want to save $3,427 for a specific purchase, you can.

- Choose your challenge format: 52-week, 100-day, or bi-weekly — pick what fits your pay schedule.

- Adjust colors and layout: Match the tracker to your home aesthetic so it looks intentional on your fridge, not like a chore chart.

- No email required: Customize and download instantly. No signup, no mailing list, no spam.

- Re-print anytime: Lost the tracker? Spilled coffee on it? Need a fresh one for a new goal? Just open the page again and print.

FAQ: Savings Challenges, Answered

How much do I need to save each week for a 52-week challenge?

It depends on the variant. The classic challenge starts at $1 in week 1 and increases by $1 per week up to $52 in week 52, totaling $1,378. The $5,000 variant starts around $51 per week and increases by $2 weekly. You can customize your own target using PrintlyTool's tracker.

Can I start the 52-week challenge mid-year?

Absolutely. The 52-week format works from any starting date — you are not tied to January 1. If you start in June, just number your weeks 1 through 52 from that date. The habit matters more than the calendar.

What if I miss a week?

Do not abandon the challenge. You have three options: (1) skip that week and accept a slightly smaller final total, (2) spread the missed amount across remaining weeks, or (3) double up the following week if you have the cash. The worst option is quitting entirely.

Is a savings challenge better than automatic transfers?

They work best together. Set up automatic transfers to move the money, and use the printable tracker as visual motivation. The automation ensures the saving happens; the tracker ensures you stay engaged.

Where should I keep the money during the challenge?

Open a separate high-yield savings account at a different bank from your checking account. The separation makes it harder to dip into savings impulsively, and the interest adds a small bonus on top of your challenge total.

What is the simplest savings challenge for beginners?

The classic 52-week challenge starting at $1 is the easiest entry point. Week 1 asks for almost nothing ($1), which builds confidence. By the time the amounts climb, you have already developed the weekly habit.

How do I stay motivated during the last few weeks?

The visual progress of a mostly-filled tracker is its own motivation. Additional tips: write your goal at the top of the tracker ("Trip to Japan — $2,500"), tell a friend about your challenge so they ask about it, and place the tracker somewhere you see multiple times a day. If you are also tracking your household budget, pair it with our pet care planning resources to see how intentional planning across categories builds financial clarity.

More Ways to Strengthen Your Financial System

A savings challenge tracker is one piece of a broader money management system. Combine it with:

- A household budget to understand where your money goes each month — use PrintlyTool's free printable household budget template

- A 52-week challenge group — find a friend or partner to do the challenge alongside you for mutual accountability

- A visual goal board — print a photo of what you are saving for and place it next to your tracker

If you are just getting started with PrintlyTool, check out our getting started guide to learn how to customize, export, and print any template. For health-related tracking, our health tracking logs guide covers blood pressure, blood sugar, and medication record templates that follow similar tracking principles.

Saving money does not require a finance degree, complex spreadsheets, or a high income. It requires a clear target, a visible tracking system, and a weekly habit. The printable savings challenge tracker handles all three. Start today — your future self will thank you for every single square you color in.