Free Printable Home Inventory Checklist for Insurance

Your apartment building catches fire. A pipe bursts and floods your basement. Someone breaks in and steals your electronics. In any of these scenarios, your insurance company will ask the same question: "Can you provide a list of everything you lost, with estimated values?"

If you are like most people, you will freeze. You will try to remember every item in every room from memory, which is impossible under stress. Studies from the Insurance Information Institute show that nearly 60% of homeowners are underinsured, and one major reason is that policyholders cannot accurately document their belongings after a loss. A printable home inventory checklist changes this — it turns a panic-inducing insurance claim into a straightforward process where you already have the answers.

This guide explains why every homeowner and renter needs a home inventory, what to include in yours, and how PrintlyTool's free customizable home inventory template lets you build a complete room-by-room record in about 30 minutes. No app download. No cloud storage worries. Just customize, print, and keep it somewhere safe.

Why Most People Skip the Home Inventory (and Why That Is a Mistake)

Ask ten people if they have a home inventory, and nine will say no. The excuses are consistent: "I do not own anything valuable," "It would take too long," or "I will do it when I have a free weekend." That free weekend never arrives — until the claim adjuster asks for documentation.

Here is what people get wrong:

- "I do not own anything valuable": Walk through your kitchen and tally the cost of a refrigerator, oven, microwave, cookware, and utensils. Then do the living room: television, sound system, furniture, books. A typical two-bedroom apartment contains $20,000 to $35,000 in personal property. A three-bedroom house often exceeds $50,000. You own far more than you think, and replacing it all out of pocket would be financially devastating.

- "My insurance covers it automatically": Most homeowners and renters insurance policies do cover personal property, but coverage is subject to limits per category. Jewelry, electronics, collectibles, and home office equipment often have sub-limits that are far lower than replacement cost. Without a documented inventory showing what you owned, the adjuster defaults to conservative estimates that rarely cover actual replacement value.

- "Photos on my phone are enough": A photo of an open closet shows clothes — it does not show brands, purchase dates, or conditions. Adjusters need specificity. A documented inventory with model numbers, serial numbers, purchase dates, and estimated values turns a vague claim into a precise one that gets paid faster and more fully.

- "Digital records are safe": Cloud storage is convenient until you forget the password, the subscription lapses, or the service shuts down. A printed inventory kept in a fireproof safe or a relative's house does not depend on any technology working when you need it most.

The Insurance Information Institute recommends updating your home inventory annually, and the National Association of Insurance Commissioners (NAIC) provides a free mobile app for this purpose — but even they acknowledge that a paper backup is essential because phones are often lost or damaged in the same disaster that destroys your home. A printed checklist stored off-site is the most reliable failsafe.

What a Complete Home Inventory Should Include

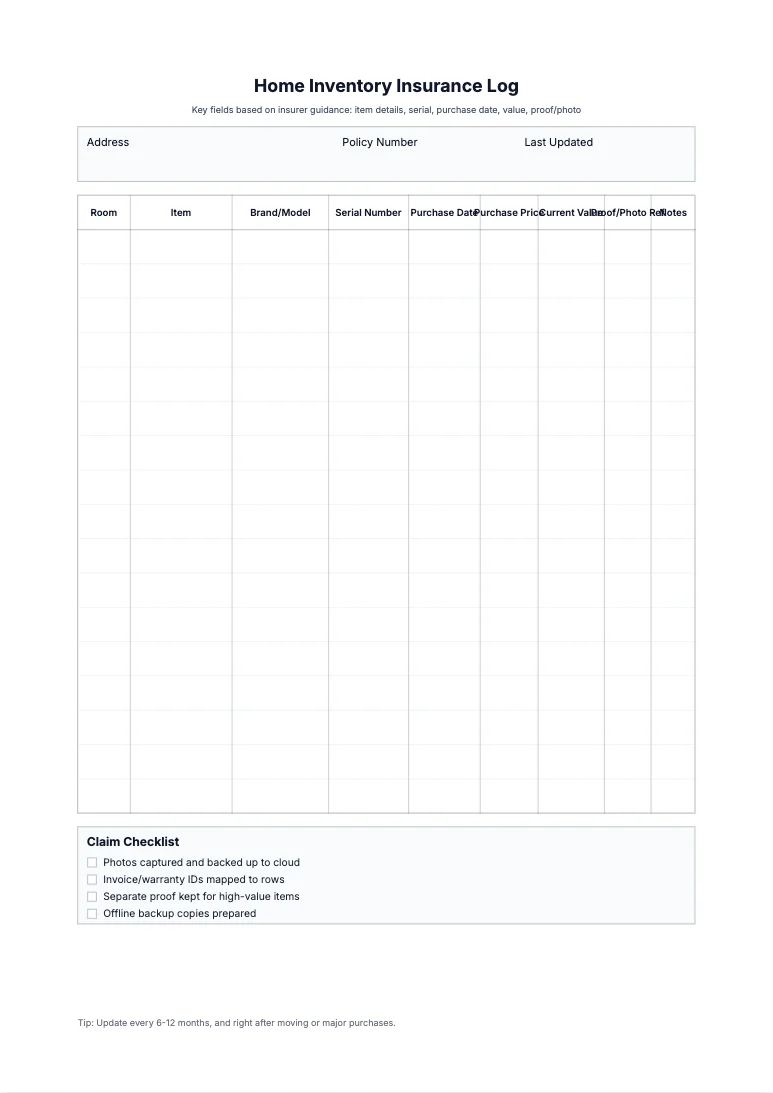

A useful home inventory is not just a list of rooms. It captures the details an insurance adjuster needs to verify and value each item. Every entry should include:

| Field | Why It Matters |

|---|---|

| Room / Location | Lets the adjuster cross-reference damage reports and ensures no area is overlooked. |

| Item Description | Be specific: "Samsung 55" QLED TV Model QN55Q80A" is better than "TV." Brand, model, and size make replacement matching possible. |

| Serial Number | For electronics and appliances, serial numbers are definitive proof of ownership. They also help police recover stolen items. |

| Purchase Date | Establishes age for depreciation calculations. A two-year-old laptop has a different replacement value than a six-year-old one. |

| Purchase Price / Estimated Value | Gives the adjuster a baseline. Include sales tax and delivery fees if you kept the receipt. |

| Receipt / Photo Reference | Note where supporting documentation is stored: "Receipt in filing cabinet drawer 2" or "Photo on external drive folder /inventory/2026/." |

| Condition | "Like new," "Good — minor scratch on left side," or "Needs repair — non-functional power button" all affect valuation. |

For categories with sub-limits — typically jewelry, fine art, collectibles, firearms, and home office equipment — include appraisals or professional valuations. Most standard policies cap jewelry at $1,500 to $2,500 per incident unless you have scheduled personal property coverage.

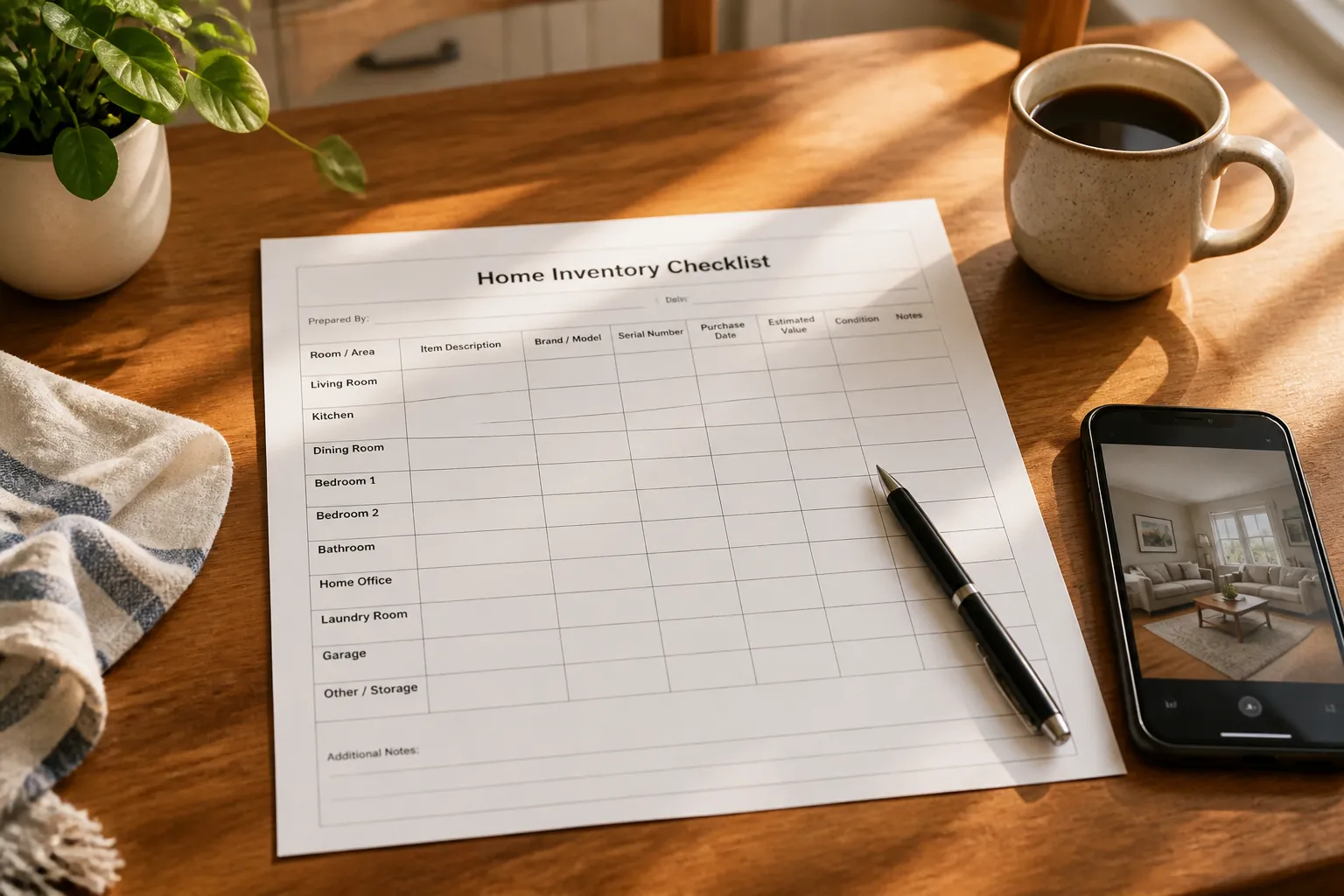

Free printable home inventory sheet for rooms, items, models, serial numbers, values, and proof references.

PrintlyTool's home inventory template includes all of these fields and lets you customize the layout before printing. You can add or remove columns, adjust the number of rows per page, change the title, and set the paper size to A4 or Letter — whatever fits your filing system.

How to Build Your Home Inventory in 30 Minutes: A Room-by-Room Method

The biggest barrier to starting a home inventory is feeling overwhelmed. Walking through an entire house cataloging every item sounds like a weekend project. But broken into a simple room-by-room method, it takes about 30 minutes for an average apartment and an hour for a house. Here is the process:

Step 1: Start with High-Value Rooms

Begin with the rooms that contain the most expensive items. For most households, that order is:

- Living room / entertainment area: Television, sound system, gaming consoles, furniture, artwork

- Kitchen: Major appliances, small appliances (coffee maker, blender, stand mixer), cookware sets, knives

- Home office: Computer, monitor, printer, desk, chair, external drives

- Bedrooms: Mattress, furniture, clothing (focus on outerwear, suits, and shoes — these add up fast)

- Garage / basement: Tools, sporting equipment, holiday decorations, storage items

- Bathrooms: Usually lower value per item, but toiletries, hair tools, and medicine cabinets collectively add up

Step 2: Use Your Phone Camera as You Go

Take a photo of each item or group of items as you record them. Open drawers and closet doors before photographing — a photo of a closed drawer proves nothing. For electronics, take a close-up of the model and serial number sticker. These photos serve as visual proof and help the adjuster identify exact replacement models.

Step 3: Record as You Unpack or Declutter

The easiest time to build an inventory is when you are already handling every item: moving into a new place, spring cleaning, or decluttering before a garage sale. You are touching everything anyway — writing it down adds only a few seconds per item.

Step 4: Store a Copy Outside Your Home

A home inventory that burns in the same fire as your belongings is useless. Keep:

- One printed copy in a fireproof safe or a safety deposit box

- One printed copy at a trusted relative's house

- A digital backup (photos of each completed page) stored in cloud storage or emailed to yourself — but do not rely on this as your only copy

For more tools to keep your household organized, see our home maintenance checklist guide and our vehicle maintenance log template, which follow the same principle: a simple paper record can save thousands in avoided costs.

Renters Insurance: Why Renters Need a Home Inventory Even More Than Homeowners

Renters often assume their landlord's insurance covers their belongings — it does not. The landlord's policy covers the building structure, not your personal property inside it. Without renters insurance and a documented inventory:

- A kitchen fire destroys your cookware, small appliances, and furniture — you pay out of pocket

- A burglary takes your laptop, gaming console, and jewelry — you have no claim to file

- A neighboring unit's water leak damages your clothing and electronics — no coverage

Renters insurance is remarkably affordable — the average premium in the United States is approximately $15 to $20 per month for $30,000 in personal property coverage, according to the NAIC. But the policy only pays out to the extent you can document what you owned. A completed home inventory is what turns a $15 monthly premium into a $30,000 payout when you need it.

For renters specifically, it is worth adding an appliance maintenance log to your household binder alongside your inventory — documenting reported maintenance issues protects you from deposit disputes when you move out.

Printable vs. Spreadsheet vs. App: Which Home Inventory Format Works Best?

Each format has trade-offs. Here is how they compare:

| Format | Pros | Cons | Best For |

|---|---|---|---|

| Printable checklist | Always accessible; no battery required; works during power outages; easy to hand to an adjuster; can store off-site physically | Requires manual updates; paper can be lost if not stored properly | Anyone who wants a reliable failsafe; older adults; people in disaster-prone areas |

| Spreadsheet | Searchable; easy to sum values; can attach photo links; shareable by email | Dependent on device and power; file can corrupt; version confusion | Detail-oriented people comfortable with Excel or Google Sheets |

| Insurance app | Convenient photo capture; cloud backup; category auto-sorting | Requires smartphone; app may be discontinued; cloud account dependency; adjusters often still ask for a printed list | Tech-savvy users as a supplement to a printed copy |

The best approach combines all three: use an app or spreadsheet to build and update your inventory digitally, then print a clean finalized copy using a customizable template and store it off-site. That printed page is the one you will actually hand to the adjuster when the power is out and your phone is dead.

How to Use PrintlyTool's Home Inventory Template

The template gives you a structured table that you can fill out room by room. Here is how to customize it for your needs:

- Title the sheet: Name it something clear like "Smith Family Home Inventory — 2026" so anyone finding it knows what it is.

- Set the number of rows: Start with 25-30 rows per page and print additional pages as needed. A typical apartment fills 2-3 pages; a house fills 4-6.

- Choose A4 or Letter: The template works with both paper sizes. Select the one your printer and filing system use.

- Customize the columns: The default template includes Room, Item, Model/Serial, Purchase Date, Value, and Notes. You can hide columns you do not need.

- Print and fill by hand: Fill in the sheet as you walk through each room. Handwriting feels slower than typing, but it forces you to physically handle and inspect each item — which is the point.

Once printed, keep the completed pages together in a durable folder or binder. Label the spine "Home Inventory" so it is easy to grab in an emergency.

For related household management, our 52-week savings challenge tracker can help you build the emergency fund that covers your insurance deductible.

FAQ: Common Questions About Home Inventories for Insurance

Do I really need a home inventory if I have replacement cost coverage?

Yes. Replacement cost coverage means the insurer pays the cost to replace items with new equivalents, but you still must prove what you owned. Without a documented inventory, the adjuster will estimate based on "average" household contents for your home size, which almost always undervalues your actual belongings. A detailed inventory gives you leverage to negotiate a fairer settlement.

How often should I update my home inventory?

At least once a year. The Insurance Information Institute recommends reviewing your inventory annually and whenever you make a major purchase — typically defined as any single item worth more than $500. Set a recurring calendar reminder for the same month you renew your insurance policy so both tasks happen together.

What items do people most often forget to include in a home inventory?

The most commonly overlooked categories are: books and media collections (a shelf of 200 books at $15 each is $3,000), clothing and shoes (a moderate wardrobe can easily exceed $5,000), kitchen gadgets and small appliances, holiday decorations, tools and hardware, children's toys, and linens and bedding. Walk through each room slowly and open every drawer and closet.

Is a video walkthrough enough for an insurance claim?

A video walkthrough is better than nothing, but it is not a substitute for a written inventory. Video makes it hard for adjusters to identify specific models and conditions. Combine a video walkthrough with a written inventory where you pause the camera at each item and record its details on paper — that combination is the gold standard recommended by most insurance professionals.

Can I use my home inventory for tax purposes?

Yes. If you experience a casualty loss — property destroyed by a federally declared disaster — you may be able to deduct unreimbursed losses on your federal tax return. A documented home inventory with purchase dates and values provides the substantiation the IRS requires. Keep your inventory with your tax records.

What should I do with my home inventory when I move?

Start fresh for the new residence, but keep the old inventory in your records for at least three years. If a previously undiscovered loss from the old property surfaces — or if you need to prove ownership of items moved from the old home to the new one — the prior inventory serves as documentation.

The 30-Minute Rule: Start Today

A home inventory feels like a chore you can put off indefinitely. But consider this: if disaster struck tonight, would you be able to list every item in your home from memory?

The solution is the 30-minute rule: commit to spending 30 minutes this week — not next month, not when you have a free weekend — walking through your home with a printed checklist and a phone camera. Start with the living room and kitchen. Even an incomplete inventory is exponentially better than no inventory at all.

PrintlyTool's home inventory template is free, customizable, and works offline. You can set the number of rows, adjust the column layout, choose A4 or Letter paper, and print a clean professional sheet in under two minutes. Combine it with our family emergency kit checklist to build a complete household preparedness binder.

A filled-out piece of paper in a fireproof safe is worth more than tens of thousands of dollars in unverified insurance claims. Start your inventory this week. Future you will be grateful.

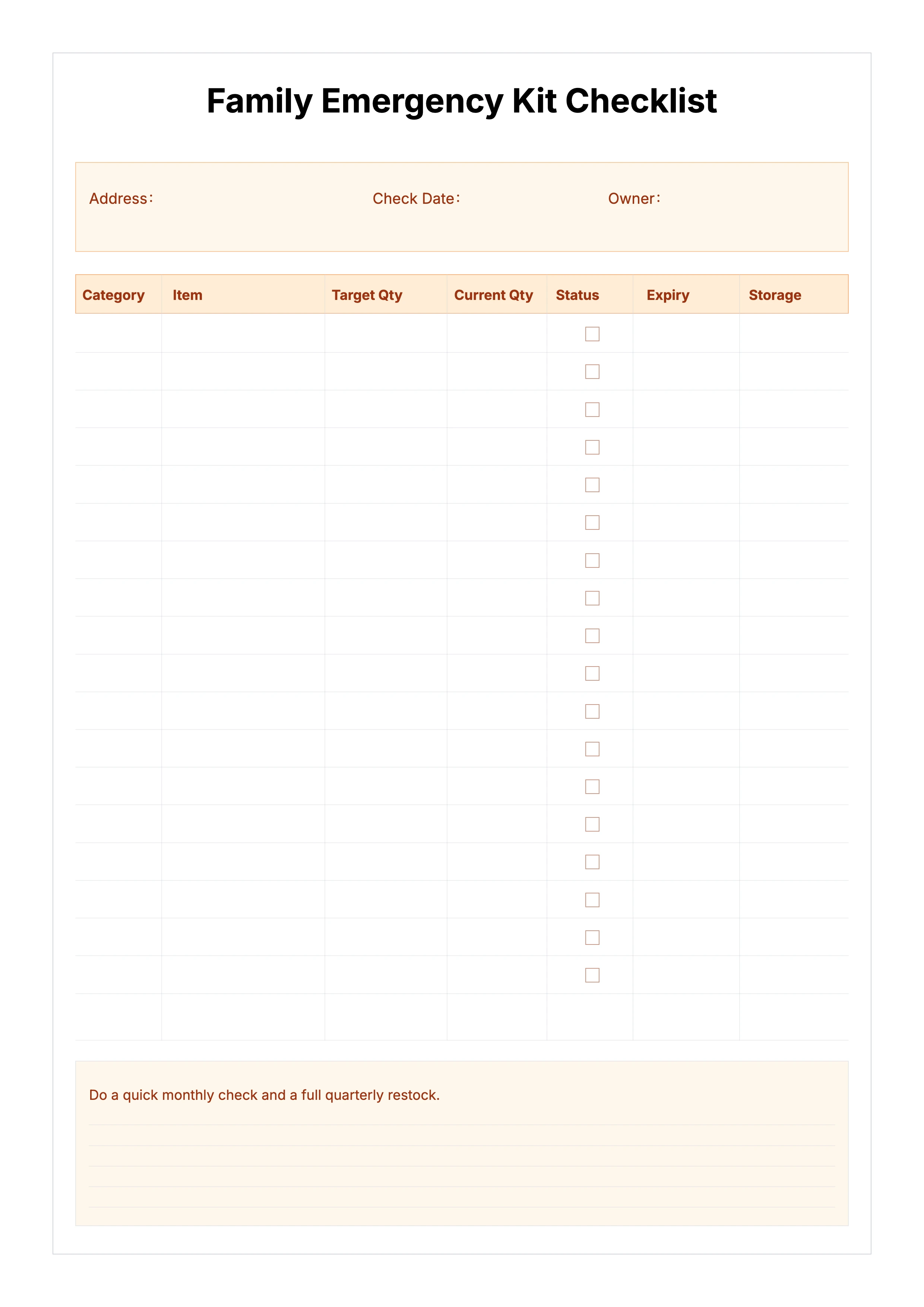

For a complete preparedness system, combine your home inventory with a ready-to-go emergency kit:

Free printable family emergency kit checklist with item category, target quantity, current quantity, expiry date, and storage location.

Keep both documents together in your household binder — when an emergency happens, you will not have to think about which drawer they are in.